Is the Stock Market Getting Ready to Crash?

Download (Login required) Audio PDF

As the second quarter of 2021 unfolds, are you a bit confused about the stock market? Do you wonder if the stock market will keep going up? Or, are we due for a correction? If there is a correction, do you fear that it may result in a complete turnaround? Are you worried about prices falling so far and so fast that it results in a crash? Are there any warning signs we can see right now?

We hear a lot of different views these days. Each side is convinced that they have the correct answer. Some people think that if the market is going up now, it will keep going up in the future. Others are continuously negative about what is happening in the US economy and say there will be a stock market crash soon. Who’s right? Who’s wrong?

Depending on who you are, you will eventually be correct if you repeatedly say the same things about the stock market. However, that doesn’t help us as we try to make decisions about our investments.

In a world that is looking for black-and-white answers, we often see gray. We want solutions that are easy to justify, conclude, and understand. Sometimes we will even overlook and dismiss valid facts just to feel that we have reached a conclusion resulting in peace of mind and confidence.

Any wise analysis must be based on reality, despite the conclusions of others. However, this leads to an even more complicated question: What is reality? As simple as this sounds, what is “real” can be a fleeting concept. I have found three powerful principles for discovering and basing decisions on reality:

- Use reliable data.

- Develop an objective interpretation of the data.

- Reach an independent conclusion.

We need to pay attention to the good (perma-bull) and the bad (perma-bear) pundits while taking things for what they are. We need to have good information sources and an effective method for applying what we learn. In the end, we need to reach our own conclusions.

Why? If used correctly, we can manage our current investments more effectively and use strategies that take advantage of any market climate (up, down, and sideways) and time frame (short, intermediate, and long-term).

There is a multitude of ways to analyze the current condition of the stock market. The number of methods can be overwhelming and confusing. Some are downright useless. New methodologies need to be constantly explored, added, replaced, and modified. I will cover just one method in this discussion.

The P/E Ratio

The Price to Earnings Ratio, or simply the P/E Ratio.

The P/E Ratio can be helpful for evaluation. How does it work? The current price of a stock or index is compared to earnings. Earnings are the backbone of any business and serve as a basis for being a desirable investment. Earnings must grow to justify any increase in share prices.

Calculating the P/E Ratio

To calculate the P/E Ratio, two pieces of information are needed:

- The current stock price.

- The Earnings Per Share (EPS).

Finding the current stock price can be found quickly by looking it up using the name or symbol. When looking for earnings, this can be a bit trickier since there are choices to make.

There are two types of earnings that can be used to calculate the P/E Ratio: Historical earnings and Future earnings.

- Historical earnings have already happened. These earnings are referred to as the Trailing Twelve Months or TTM.

- Future earnings often receive the most attention and are the most riveting for investors. The stock market looks forward, not backward, when setting current prices. Wall Street is full of thousands of analysts who try to figure out future earnings. Many individual investors love to “crunch the numbers” and come up with their own value. Sometimes the calculations are right, and sometimes they are wrong. Those who implement this approach call this Fundamental Analysis.

However, for this discussion, TTM, based on historical earnings, will be used.

Why TTM? It only stands to reason that if current prices are based on future expectations, shouldn’t that be the focus? Yes, that does have a place and is used. But seeing what has happened historically can also have great analytical value.

TTM numbers are real and official, whereas future earnings are forecasts or guesses. TTM earnings can be used as a gauge to measure current conditions by comparing them to what has happened previously. History may not exactly repeat itself, but it does rhyme. The past can often help guide us into the future.

TTM numbers are based on GAAP or Generally Accepted Accounting Principles (there are acronyms aplenty in the stock market, as with most everything in life). In other words, earnings reports for the last year, calculated according to current industry standards, are the numbers I will use.

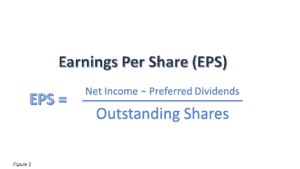

Another concept that morphs into an acronym is called Earnings Per Share, or EPS. Simply put, the EPS is calculated by dividing profits by the outstanding shares of stock. The result demonstrates the profitability of a company. The keyword is profits. Companies that do not have profits do not have a positive P/E Ratio. Refer to Figure 1.

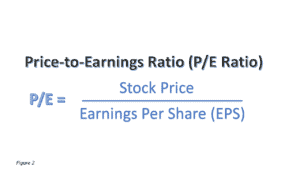

When the P/E Ratio is calculated this way, the current stock price is divided by the EPS. See Figure 2.

Multiples

Here’s where things can get a bit hazy. Investors are not satisfied with just using the current EPS number. Since the stock market is forward-looking, the EPS is viewed as a multiple of 10, 15, or 20. We can see what the stock market thinks the value should be right now based on this multiple.

Why is it multiplied by 10, 15, or 20? If a company’s earnings are expected to grow in the future, people will want to invest in that stock. Stated another way, a multiple of 10 means it will take 10 years of the same profits for a stock to equal the current share price.

Whether this makes logical sense or not, it is what happens in the stock market. Over a period of time, Wall Street has come up with numbers that are considered to be:

- Expensive

- Cheap

- Fairly Valued

This “Goldilocks approach” to investing has been implemented by millions of investors for hundreds of years and is today’s dominant approach.

Using a P/E Ratio for a stock

If the TTM EPS is a multiple of 10, the resulting value is considered cheap. If the current price is at or below this value, an investor will want to buy this stock.

If the TTM EPS is a multiple of 15, the resulting value is considered fair or just right. If the current price is near this value, an investor may want to hold onto this stock.

If the TTM EPS is a multiple of 20, the resulting value is considered to be expensive. If the current price is at or above this value, an investor may want to sell this stock if it is already owned or stay away if looking to buy.

Using a P/E Ratio for an Index

The same approach can be applied to an index, such as the S&P 500. All of the TTM EPSs are added up and divided into the current value of the index. The same analysis can be used to determine if the index is inexpensive, at fair value, or expensive.

Using P/E Ratios to Make Decisions

As numerous “experts” appear in the media, they may state that they think a stock or an index is “cheap, fairly-priced, or expensive.” This statement usually comes from analyzing the current P/E Ratio based on their method for performing the calculations. Investors often use the P/E Ratio when looking to buy, sell, or hold a stock or an index.

An Expensive Index

If prices become expensive, does that mean you need to freak out right now? Not necessarily. An over-priced stock market is a situation that can go on for an extended period of time. Prices can deviate from fair value for weeks, months, and even years. Hence, investors don’t have to decide right away after discovering that current prices are expensive. However, it is always good to be thinking about what should be done and when to do it. Having a plan can be a good thing. When looking at executing a well-thought-out plan, it is common for other types of analysis tools to be used to help determine when it is time to sell.

When an investor gets to the point of feeling consistently uncomfortable, changes may be in order. Other measures may be needed, such as implementing protection or hedging.

Making Comparisons

The chart below is something investors should always keep an eye on. The chart represents the closing values for the S&P 500 (SPX) going back to 1990.

As stated earlier, a P/E Ratio can be calculated for a stock, as well as for an index. Often, investors find this useful when comparing a stock to an index to see if it’s overvalued, undervalued, or at fair value. This gives investors a point of reference for comparison.

For example, an investor sees that the current P/E Ratio of a stock is 20. What does that mean? Is that a big number, small number, or a number at fair value? If an index representing the stock is at 15, quick comparisons can be made relative to the broader market.

Chart Analysis

NOTE: I have made the S&P 500 reference levels near whole numbers and calculations results simple for all examples that use charts. The chart changes daily, but the concept does not. The idea is to understand the concept without fretting over exact numbers.

In addition to closing prices, the displayed chart also shows three different calculations. On the bottom is a green dotted line. This line is calculated by plotting the P/E Ratio by a multiple of 10. On the chart, this value is at about 1,000.

The next dotted line is blue. This line is considered fair value after plotting a multiple of 15. Throughout history, a multiple of 15 has been pretty good at classifying when an index is not overvalued or undervalued. Fair value for the SPX is currently just under 1,500.

Next is a dotted red line. This expensive level suggests that the SPX should be around 2,000.

Just to summarize things, if the SPX is near 4,000, this means:

- The SPX would need to decline 50% to be expensive.

- The SPX would need to decline 62.5% to be at fair value.

- The SPX would need to decline 75% to be cheap.

Does this give you any grounds for concern? Looking back in time, there were periods when the stock market was cheap, other times when it was at fair value, and other times when it has been expensive. Sooner or later, prices must respond to the reality of earnings.

In 1987, the SPX crashed all the way back to fair value. Then, the market started to recover, and prices stayed at fair value for a few years.

In the late 1990s and early 2000s, the Dot-Com tech boom and bust happened. During that time, prices shot up, and the SPX became expensive. The party eventually ended because the earnings needed to justify the higher prices didn’t exist. Prices fell and got closer to fair value. Then 9-11 happened. That decimated the economy for a few years and took the stock market with it.

Finally, in 2003, the SPX started to recover. From 2003-2007 things were looking good again. Sadly, another major meltdown occurred in 2008 with the housing crisis. Everything tanked again.

The EPS in 2008 had become unjustified. It took some time, but eventually, reality caught up with fantasy. Company earnings declined, and the SPX earnings as a whole turned negative. That’s why the chart looks strange during that period. After a few years, things started to recover, there was a bounce up to fair value, and prices began to climb.

Up to 2020, earnings went up, and so did the SPX. But things became pretty expensive. There were some pullbacks along the way, but the overall uptrend continued.

Then, the COVID-19 Pandemic hit, and things have yet to resume any kind of consistent normalcy, based on history.

When the SPX gets too far from the TTM EPS values, something needs to happen to bring things back in line. Three things can happen:

- Earnings must go up to justify the lofty price level of the SPX.

- Prices must fall and get back to a closer-to-normal valuation level.

- A combination of 1 and 2.

The COVID-19 breakout has thrown the whole US economy into turmoil, where it remains to this day. The US economy is still trying to figure out where things go from here. Numerous outcomes have been hypothesized. What will happen is yet to be determined. Any dogmatic declaration, either up or down, should be taken with a healthy dose of skepticism.

In the meantime, corporate earnings have plunged while the US economy is attempting to recover from being shut down. Fiscal (Congress) and monetary (The Federal Reserve) policies have been enacted to try and keep the US economy alive. These policies have added unprecedented amounts of liquidity to the economy. Additionally, stimulus checks have provided unbridled funds to flow, potentially, into the economy. Inflation, hyperinflation, stagflation, and deflation may occur in the future.

The increase in liquidity by the Fed is introduced into the economy through the bond market. Some of these funds often find their way into the stock market. Additionally, the stimulus checks sent to individuals have allowed at least some funds to go into the stock market. This influx of cash has kept prices climbing to stratospheric levels.

Until things are worked out, there is a real strong disconnect between where the SPX is and where the SPX should be based on historical values. At some point, the SPX will need to decline, or corporate earnings will need to increase. Until that happens, all scenarios are viable.

Again, does this mean investors should panic? No. Panic forces emotionally-based decisions that are almost always wrong or imprudent at best. However, this does mean investors should keep a close tab on things and have a plan in place if the stock market starts to head aggressively lower. If investors wait until prices start falling to develop and execute a plan, it may be too late.

A second chart, the same as the first chart, adds an additional calculation to provide another graphical example. The value of the red line (expensive) is subtracted from the current value of the SPX. The green and blue lines have been ignored since these levels are currently irrelevant. The SPX is exponentially further away from earnings levels than at any time in modern US history.

There are indeed numerous changes taking place all over the world. There is talk of a great “reset.” Some are excited about what that means, while others see it as impending doom. Whether that’s going to be positive or negative is yet to be seen. Things need to play out. However, investors need to be prepared no matter what happens.